The Comprehensive Guide to Master Tax Benefits on Home Loans: All You Need to Know

Owning a home is often regarded as a symbol of stability, security, and accomplishment. However, home ownership is a major financial commitment that can strain your finances, and comes with its own set of financial implications. To make it easier for home buyers, the Indian Government offers financial relief in the form of tax benefits on home loans.

The provisions embedded in specific Sections in the Income Tax Act, 1961 grant deductions on both principal and interest amounts paid on home loans. These tax benefits can substantially reduce your taxable income.

Jump to: Table on Tax Benefit on Housing Loan

In this blog, we have uncovered the intricacies of various tax benefits you can avail on home loans, and explained how each Section relevant to housing loan in the Income Tax Act can play a pivotal role in your home ownership journey.

Let's dive right in.

Also Read: What are the Home Loan Eligibility Criteria?

Tax Benefits on Home Loans under Various Sections of Income Tax Act, 1961

The Income Tax Act, 1961 (I-T Act), has distinct sections earmarked to offer substantial tax benefits on home loan, namely Section 24, Section 80C, Section 80EE, and Section 80EEA. Each of these sections has its own set of benefits, eligibility criteria, and conditions.

Whether you're a first-time homebuyer or someone considering refinancing, understanding these provisions can be your key to unlocking significant tax savings.

Also Read: All Financial Real Estate Terms Related to Home Loans

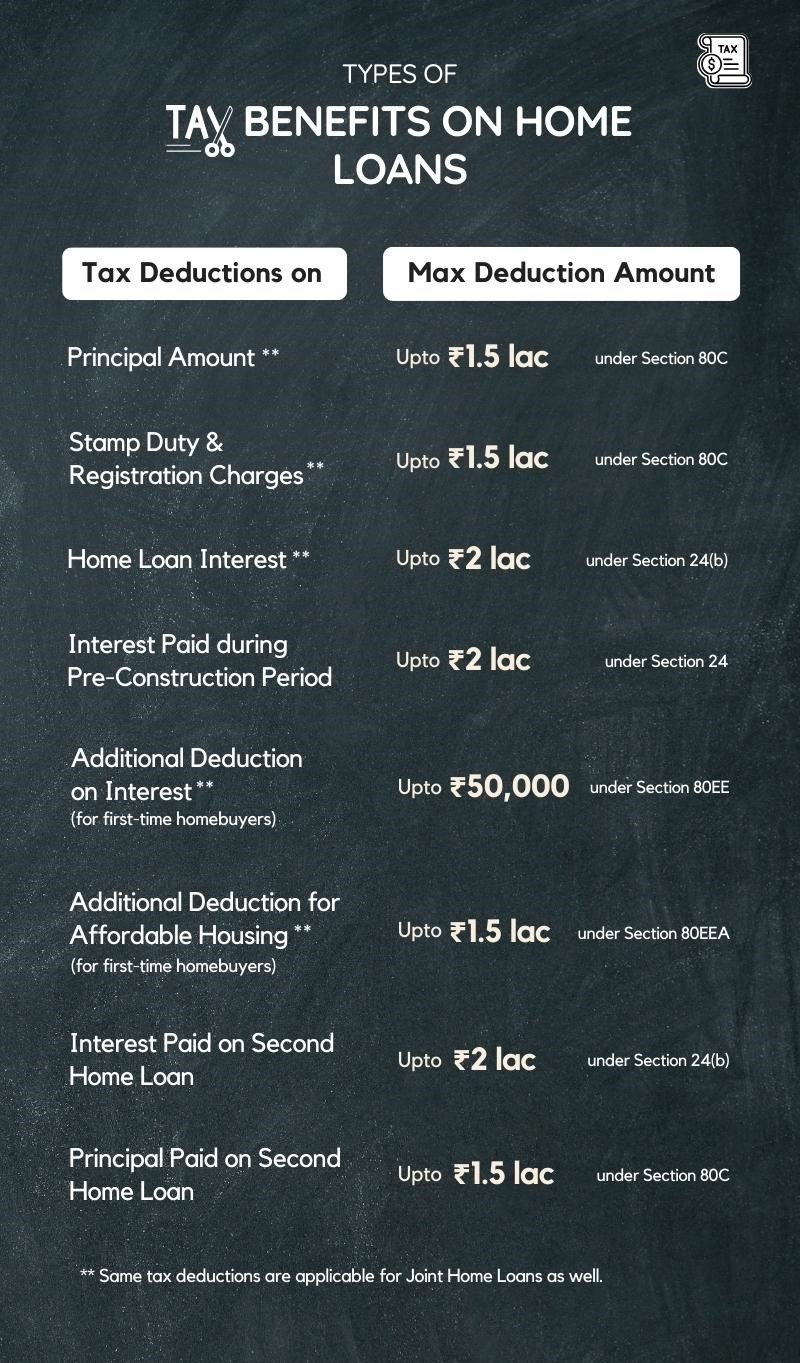

| Deductions On | Max Deductible Amount | Section & Eligibility Criteria |

|---|---|---|

| Principal Amount | ₹1.5 lakhs (across all eligible investments/ expenditures u/s 80C) | Section 80C (Check Eligibility) |

| Stamp Duty & Registration Charges | ₹1.5 lakhs (across all eligible investments/ expenditures u/s 80C) | Section 80C (Check Eligibility) |

| Interest Amount | ₹2 lakhs (self-occupied property) | Section 24(b) (Check Eligibility) |

| Total Interest Paid (rented property) | ||

| ₹30,000 (reduced limit) | ||

| Interest Paid during Pre-construction | ₹2 lakhs (self-occupied property) | Section 24 (Check Eligibility) |

| Total Interest Paid (rented property) | ||

| ₹30,000 (reduced limit) | ||

| Additional Deductions | ₹50,000 (First Time Home Buyers) | Section 80EE (Check Eligibility) |

| Additional Deductions for Affordable Housing | ₹1.5 lakhs (First Time Home Buyers) | Section 80EEA (Check Eligibility) |

| Joint Home Loans | ₹2 lakhs Each (Interest Deduction) | Section 24(b) (See details) |

| ₹1.5 lakhs Each (Principal Deduction) | Section 80C (See details) |

|

| ₹1.5 lakhs Each (Stamp Duty & Registration Deduction) | Section 80C (See details) |

|

| ₹50,000 Each (Additional Deductions for First Time Home Buyers) | Section 80EE & 80EEA (See details) |

₹1.5 lakhs Each (Additional Deductions for Affordable Housing) |

| Second Home Loan | ₹1.5 lakhs (Principal Deduction) | Section 80C (See details) |

| ₹2 lakhs (Interest Deductions for Self-occupied/ Vacant Property) | Section 24(b) (See details) |

|

| Total Interest Paid (Interest Deductions for Rented Property) |

Also Read: The Ultimate Guide to buy a New Home

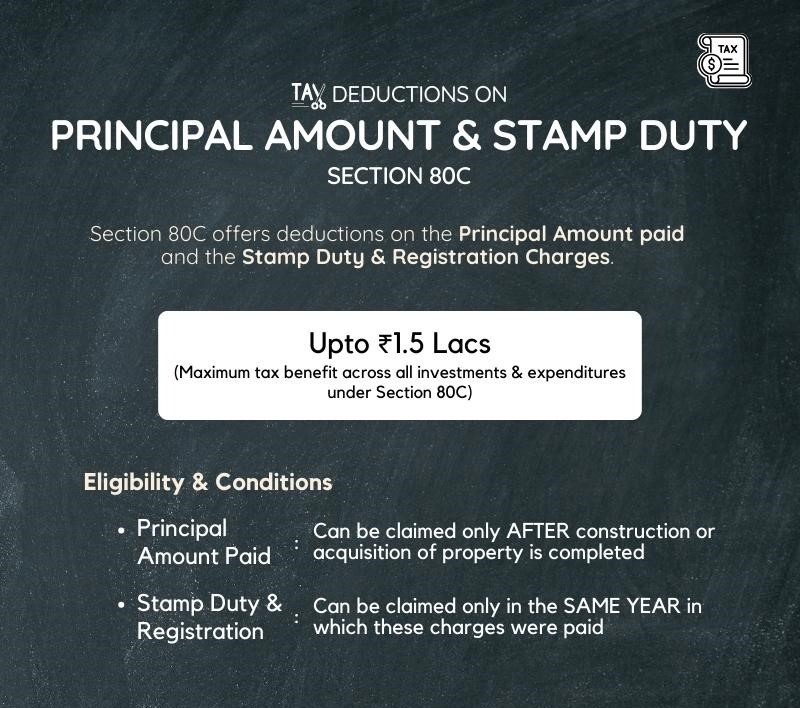

Tax Deductions on Principal Amount & Stamp Duty and Registration Charges (under Section 80C)

Among the various sections of the Income Tax Act, 1961, Section 80C stands out as one of the most widely recognized and availed.

What is Section 80C?

Section 80C is a provision in the I-T Act, 1961, that allows taxpayers to claim deductions every year on their total income, from various investments and expenditures eligible for tax deduction like investments in Provident Funds (PPF, EPF, etc.), Life Insurance Premium payments, mutual funds, pension plans, NPS, Atal Pension Yojana, etc.

#1 Maximum Tax Deduction on Principal Amount u/s 80C

Tax deductions on payments made towards the principal repayment of a home loan not only helps the taxpayer reduce their home loan burden year on year, but also decreases their tax liability.

A maximum of ₹1.5 lakh can be claimed as deduction (across all eligible investments and expenditures u/s 80C).

Eligibility & Conditions to Claim Tax Benefit on Principal Amount

For taxpayers to be eligible and avail the tax benefit on the principal paid under Section 80C, the following conditions need to be met:

-

Tax exemption u/s 80C is applicable only to individual taxpayers and Hindu Undivided Families. Businesses, corporate bodies, and partnership companies are not allowed to claim tax deductions u/s 80C.

-

If the property is jointly owned and the loan is co-borrowed, each co-owner can claim the tax deduction proportionate to their share.

-

The deduction for principal repayment can only be claimed once the construction of the property is complete.

-

Any principal repayments made during the construction period are not eligible for deduction under this section.

-

If the property is sold within 5 years from the end of the financial year in which possession was obtained, the deductions claimed u/s 80C for principal repayments in the previous years will be added back to the income in the year of sale and will be taxable.

#2 Maximum Deductible Amount for Stamp Duty & Registration Charges u/s 80C

When buying a property, stamp duty (tax paid on the transaction document) and registration charges (fees for recording the document) are considered as the two largest expenses made, apart from the property's price.

Few people are aware that Section 80C also caters to deductions for stamp duty & registration charges.

Up to ₹1.5 lakh can be claimed in a financial year (this deduction encompasses various investments/expenditures like EPF contributions, life insurance premiums, principal repayment of home loans, etc., along with stamp duty and registration charges).

Eligibility & Conditions to Claim Deduction

To avail the tax benefit on stamp duty and registration charges u/s 80C, these conditions must be fulfilled:

-

Deduction for stamp duty and registration charges can be claimed for any residential property, be it a house or a flat.

-

The deduction can be claimed only in the year in which these charges are paid. If you paid these charges in a particular financial year, you cannot claim this tax deduction in subsequent years.

-

Only individuals or Hindu Undivided Families (HUF) can claim this deduction. Corporate entities, partnership firms, etc., are not eligible.

-

While determining the property value for capital gains (and subsequently capital gains tax), in the future, these charges won't be included in the cost of acquisition if they have already been claimed as a deduction u/s 80C.

E.g., Mr. Sharma bought an under-construction property in 2020 with the help of a home loan. In the same year, he claimed the stamp duty & registration charges and started paying EMIs on the loan immediately. Construction of the property was completed in 2022. From the year 2022, Mr. Sharma started claiming deductions on the principal amount of his EMIs under Section 80C, reducing his taxable income by up to ₹1.5 lakh annually.

Also Read: When Should You Do Legal Verification of a Property?

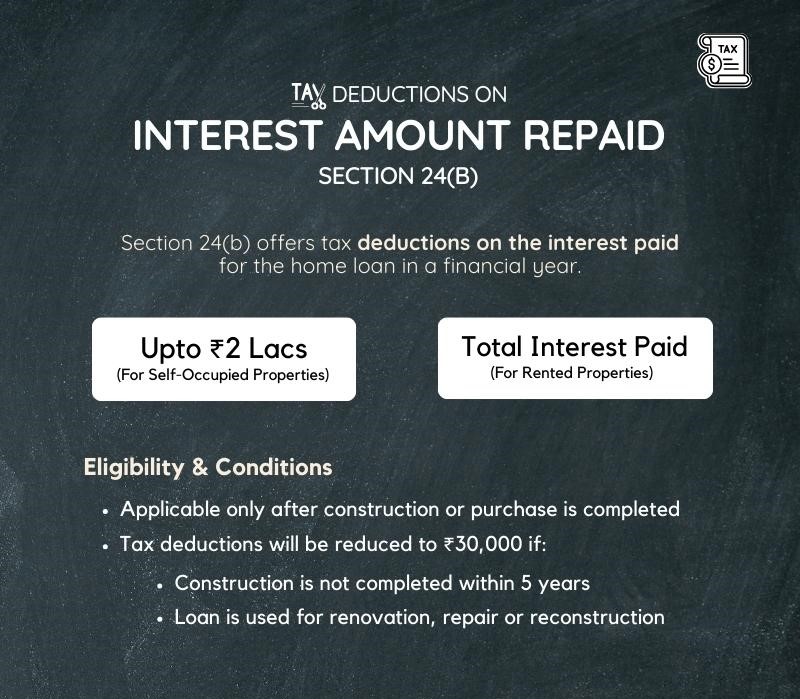

Deductions on Interest Paid on Home Loans (under Section 24B)

While the principal repayment gets a deduction under Section 80C, Section 24(b) specifically provides housing loan tax benefit to homeowners on the interest they pay.

What is Section 24(b)?

Section 24(b) makes a provision for tax deductions on the interest paid on home loans taken for the purchase, construction, repair, or renovation of a residential property. This provision was introduced to reduce the financial strain on homeowners who often find themselves paying substantial amounts as interest over the tenure of their loan.

Maximum Tax Deductible on Interest Payments u/s 24(b)

-

For Self-Occupied or Vacant Property: A maximum amount of up to Rs 2 lakh can be claimed as housing loan interest deductions, i.e.,

-

If the interest paid is less than Rs 2 lakh, then the lower amount can be availed as tax benefit (e.g., if interest amount is ₹1.3 lakh, then deduction allowed will be ₹1.3 lakh);

-

If the interest paid is more than Rs 2 lakh, only Rs 2 lakh deduction can be claimed (e.g., if interest amount is ₹2.3 lakh, then deduction allowed will be ₹2 lakh).

-

-

For Properties that are Rented Out: As per the revised rules of Finance Act, 2017, the complete interest paid on the home loan can be claimed, without any capped/upper limit.

-

If the home owner lives in another city for business or employment (in a rented property), then the tax deduction for interest on housing loan can be claimed only up to ₹2 lakh.

-

Eligibility & Conditions to Avail Max Deductions u/s 24(b)

-

The deduction can be claimed for self-occupied, vacant and rented properties.

-

The home loan must be taken on or after April 1st, 1999 for the purchase or construction of a property.

-

Tax benefits of Section 24(b) will NOT be applicable on loans taken to purchase land or to pay brokerage or commission to an agent.

-

-

The deduction on the interest is applicable only after the construction is complete or the property has been acquired.

-

If the property is still under construction, the interest for that period can be aggregated and claimed in five equal installments starting from the year of completing the construction or purchase.

-

-

In case of a joint loan, both borrowers can claim the interest paid on the home loan, but it should be in proportion to their ownership in the property.

Deduction will be reduced to ₹30,000 in the following circumstances:

-

if the construction or purchase is not completed within 5 years from the end of the financial year in which the loan was taken.

-

if the loan is borrowed on or after April 1st, 1999, for repair, renewal, renovation, or reconstruction of a property.

-

if the loan is borrowed before April 1st, 1999, for the purchase or construction of a property.

Note: To verify details of the interest repayment, a valid home loan interest certificate by the lender is necessary, which specifies the amount of interest paid during the financial year.

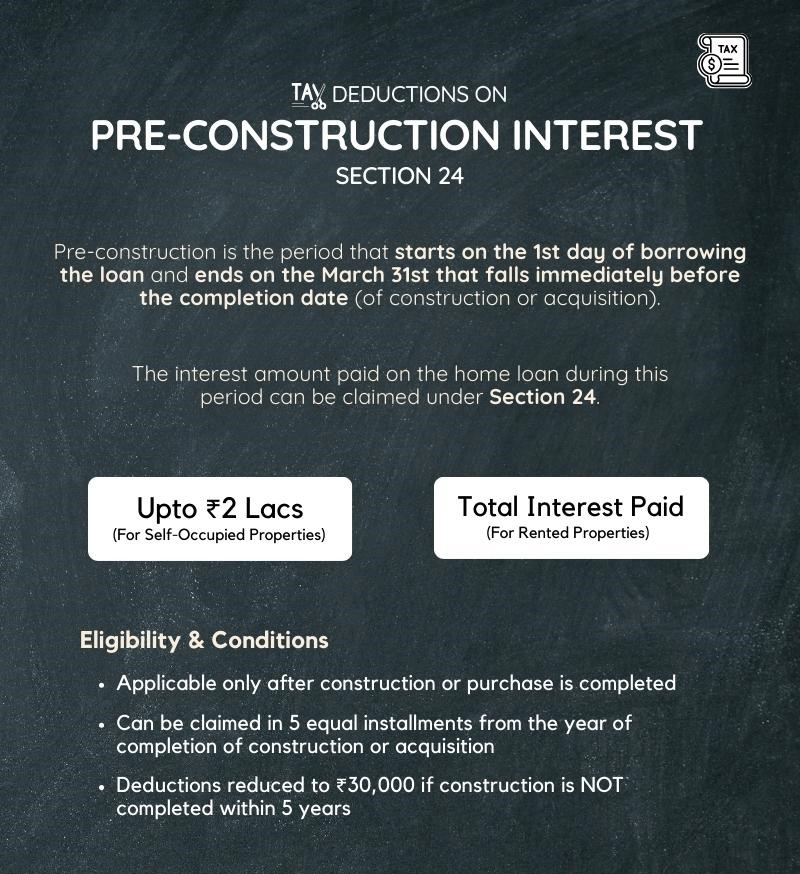

Deduction on Interest Paid During Pre-construction Period (under Section 24)

If you have purchased a property that is still under construction, and you have started paying the EMIs before the property is ready for possession, you can claim tax deduction for the interest paid during this period — also known as the 'pre-construction period'.

Pre-construction period is defined as the time starting on the date of borrowing the loan and ending on March 31st that falls immediately prior to the date of completion of construction or acquisition.

Maximum Pre-Construction Interest Deductible

The interest accumulated during the pre-construction period is deductible in five equal installments every year AFTER the compeltion of construction or acquisition.

This deduction is separate from the eligible deduction you can claim under Section 24(b), however, the maximum tax deduction is capped at ₹2 lakhs.

-

For a self-occupied property: As specified under Section 24 of the I-T Act, the deduction for interest during the pre-construction period is included in the overall limit of ₹2 lakhs per annum.

-

For let-out property: The entire interest is deductible, but any loss in income that can be claimed under the head 'Income from House Property' is capped at ₹2 lakhs.

Eligibility & Conditions to Avail Pre-construction Interest Deductions

-

The deduction can be claimed in five equal annual installments, beginning from the year in which the construction is completed or property is acquired. It's over and above the interest for the respective financial year.

-

This deduction is applicable to self-occupied and let-out properties. However, the limits on deductions vary based on the use of the property.

-

The maximum amount of deduction is reduced to ₹30,000 if the construction or acquisition of the property is NOT completed within 5 years from the end of the financial year in which the loan was taken.

-

Unlike the immediate deduction on home loan interest under Section 24(b), the deduction for pre-construction interest doesn't fall under any particular section. It's considered part of the overall interest deduction allowed under Section 24 of the I-T Act.

E.g., Ms. Chatterjee bought an under-construction property in 2018, with possession in 2022. She had paid ₹3 lakhs as interest during the pre-construction period. From 2022, apart from the regular interest deduction, Ms. Chatterjee started claiming ₹60,000 (1/5th of ₹3 lakhs) annually for the next five years under Section 24.

Also Read: Why is it a Good Idea to Invest in Real Estate?

Additional Deductions for First Time Home Buyers (under Section 80EE)

To encourage home ownership further, the Govt. introduced Section 80EE that offers an added layer of tax benefits specifically designed for first-time homebuyers.

What is Section 80EE?

Section 80EE provides additional tax deductions on the interest paid on home loans along with the deductions claimed u/s 24. This provision aims to increase the growth of the housing sector by making home buying more financially appealing for first-timers.

Maximum Interest Deduction under Section 80EE

A total tax deduction of up to ₹50,000 per financial year can be claimed on the interest paid on the home loan.

[Along with the Rs 2 lakh deduction claimed u/s 24(b), this additional ₹50,000 deduction u/s 80EE can result in an overall potential tax benefit of up to ₹2.5 lakhs for first-time homebuyers.]

Eligibility & Conditions for Claiming Deduction u/s 80EE

-

This home loan tax benefit is exclusively for individuals buying a house for the first time. If the taxpayer or their spouse already owns a house, they won't be eligible.

-

The home loan amount should NOT exceed ₹35 lakhs.

-

The value of the property should NOT exceed ₹50 lakhs.

-

Only individuals can avail this tax benefit; HUF (Hindu Undivided Families), AOP (association of Persons), Corporate Companies, etc., are not eligible to claim tax deductions.

-

The loan must have been sanctioned between or during FY 2013-14, FY 2015-16, FY 2016-2017. (At the time of loan sanction, the individual should not own any other properties)

-

The deduction under this section is available until the repayment of the loan, provided all other conditions are consistently satisfied.

E.g., Ram took a home loan in 2017 for a property worth ₹40 lakhs with an annual interest of ₹2.5 lakhs. Besides the standard deduction under Section 24, Ram also claimed an additional ₹50,000 under Section 80EE, getting the maximum benefit as a first-time homebuyer.

Also Read: How to Evaluate the Value of Your Property Correctly

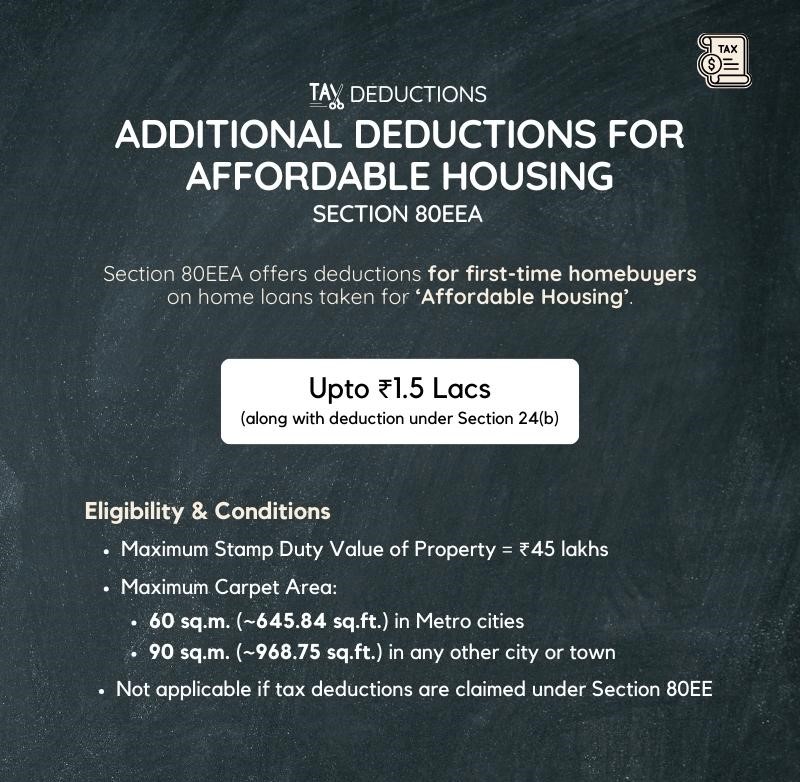

Additional Deductions on Interest for Affordable Housing Loans (under Section 80EEA)

The Govt introduced Section 80EEA in 2019 (as an addition to section 80EE) to make housing accessible to a larger segment of the population.

What is Section 80EEA?

Section 80EEA helps first-time homebuyers to purchase 'affordable housing' which has a property value of up to ₹45 lakhs along with certain carpet area requirements according to the city in which the property is purchased.

Maximum Tax Deduction under Section 80EEA

Up to ₹1.5 lakhs on the interest paid on their home loans can be claimed by first-time homebuyers.

[This tax deduction can be availed along with the tax benefit of ₹2 lakh interest deduction permissible under Section 24(b), resulting in an overall tax deduction of ₹3.5 lakhs.]

Eligibility & Conditions to Claim Tax Benefits u/s 80EEA

-

The stamp duty value of the property should NOT exceed ₹45 lakhs.

-

The carpet area of the property must NOT exceed:

-

60 sq.m. (~645.84 sq.ft.) in metropolitan cities (Bengaluru, Mumbai, Chennai, Hyderabad, Kolkata, Delhi, Gurgaon, Faridabad, Ghaziabad, Noida, and Greater Noida);

-

90 sq.m. (~968.75 sq.ft.) in any other city or town.

-

-

This deduction is specifically tailored for individuals purchasing a house for the first time.

-

The home loan must have been sanctioned during FY 2019-20, FY 2020-21, FY 20212-22 to be eligible for this deduction. (At the time of loan sanction, the individual should not own any other properties)

-

If an individual is claiming deductions under Section 80EE, they CANNOT claim deductions under Section 80EEA for the same property. However, if the taxpayer is eligible for both, they should opt for Section 80EEA due to its higher deduction limit.

-

The deduction under this section can be claimed until the entire loan is repaid, or for a maximum of 7 years, whichever is earlier, given all other conditions are consistently met.

-

In case of joint loans, both co-borrowers can claim for tax deduction, but one of them have to meet the criteria and conditions to avail the tax benefit.

E.g., In 2021, Mr. Khan took a home loan for a property whose stamp duty value was ₹42 lakhs. His annual interest for the loan was ₹2.8 lakhs. On top of the ₹2 lakhs deduction under Section 24, Mr. Khan claimed an additional ₹1.5 lakhs under Section 80EEA, thus reducing his taxable income by a total of ₹3.5 lakhs.

Also Read: Which is Better to Buy: Freehold Property or Leasehold Proeprty?

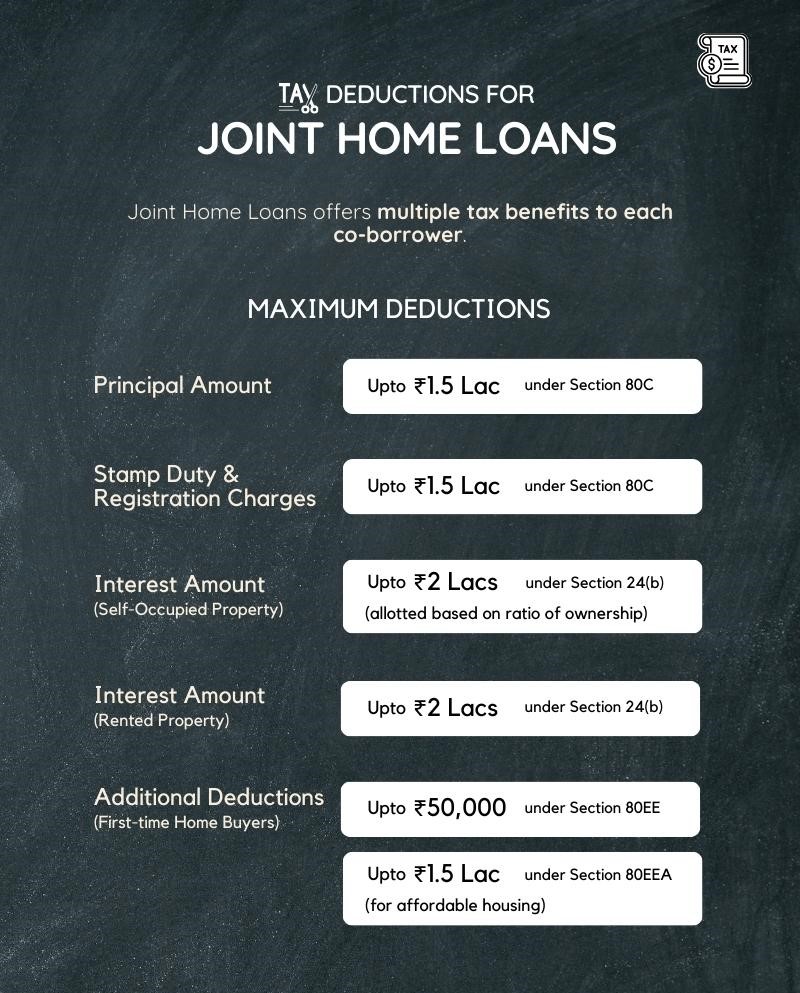

Joint Home Loan Tax Benefits

Joint home loans have become increasingly popular. Besides improving loan eligibility, joint home loans offer multiple tax benefits, making them a preferred choice for many.

What is a Joint Home Loan?

A joint home loan is essentially a housing loan that is taken by two or more individuals together. Commonly availed by spouses, parents and children, or even siblings, this arrangement is typically opted for when the loan amount required is substantial, and it's financially strenuous for a single individual to bear the debt.

Income Tax Benefit on a Joint Home Loan taken by Co-borrowers

#1 Deductions on Principal Amount Paid

Under Section 80C, each co-borrower can avail a deduction up to a maximum limit of Rs 1.5 lakh for repayment of the principal portion of the home loan.

#2 Deduction on Stamp Duty and Registration Charges

Co-borrowers can also claim tax deduction on stamp duty and registration charges under Section 80C, within its overall ceiling of ₹1.5 lakh.

#3 Interest Claim on the Joint Home Loan

For a self-occupied property: Each co-borrower can claim a deduction of up to Rs 2 lakh on the interest paid on the home loan (under Section 24) in their Income Tax Return. The total interest paid will be calculated or allocated to the co-owners based on their ratio of ownership in the property.

E.g., if Sumit and his father take a home loan together to purchase a house with 50:50 ownership, and pay a total interest of ₹5 lakhs on the home loan, each of them will be eligible for a tax deduction of ₹2 lakhs in their respective IT returns.

For a rented property: The interest that can be claimed as deduction for a rented property can go up to the point where the loss from the property does not exceed ₹2 lakhs.

#4 Additional Income Tax Deduction

If the co-borrowers are first-time homebuyers, they can also save tax from the deductions of up to ₹50,000 under Section 80EE. Moreover, for purchasing affordable housing, the benefits of ₹ 1.5 lakhs under Section 80EEA can be availed.

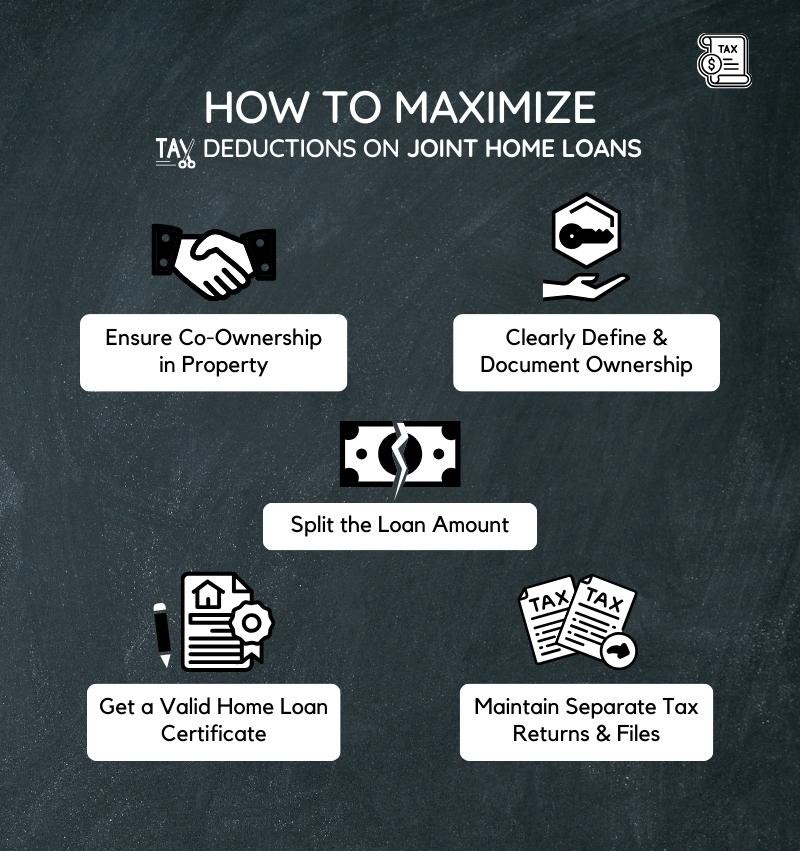

How to Maximize Tax Deductions with Joint Home Loans

E.g., Mr. and Mrs. Fernandes took a joint home loan, both being co-owners and co-borrowers. Their annual interest was ₹3.8 lakhs and principal repayment was ₹2.6 lakhs. Both claimed up to ₹2 lakhs for interest and up to ₹1.5 lakhs for principal repayment individually, maximizing their combined tax benefits.

-

Ensure Both are Co-owners of the Property: To avail tax benefits, it's essential that both the co-borrowers are also co-owners of the property. Being just a co-borrower without ownership doesn't qualify one for tax deductions on joint hoem loans.

-

Clear Ownership Documentation: Make sure that the property's ownership share is clearly defined and documented. The tax benefits are generally in proportion to each co-borrower's share in the loan and property.

-

Split the Loan Amount: Make sure both borrowers have a significant share in the loan. This way, both can claim substantial deductions individually, thereby reducing their overall taxable income considerably.

-

Valid Home Loan Interest Certificate: It's crucial to have a certificate from the lending institution, indicating the share of each co-borrower in the principal and interest amounts.

-

Maintain Separate Tax Files: Both co-borrowers should file their tax returns separately to claim their respective tax deductions.

Also Read: Advantages & Disadvantages of Owning a Home

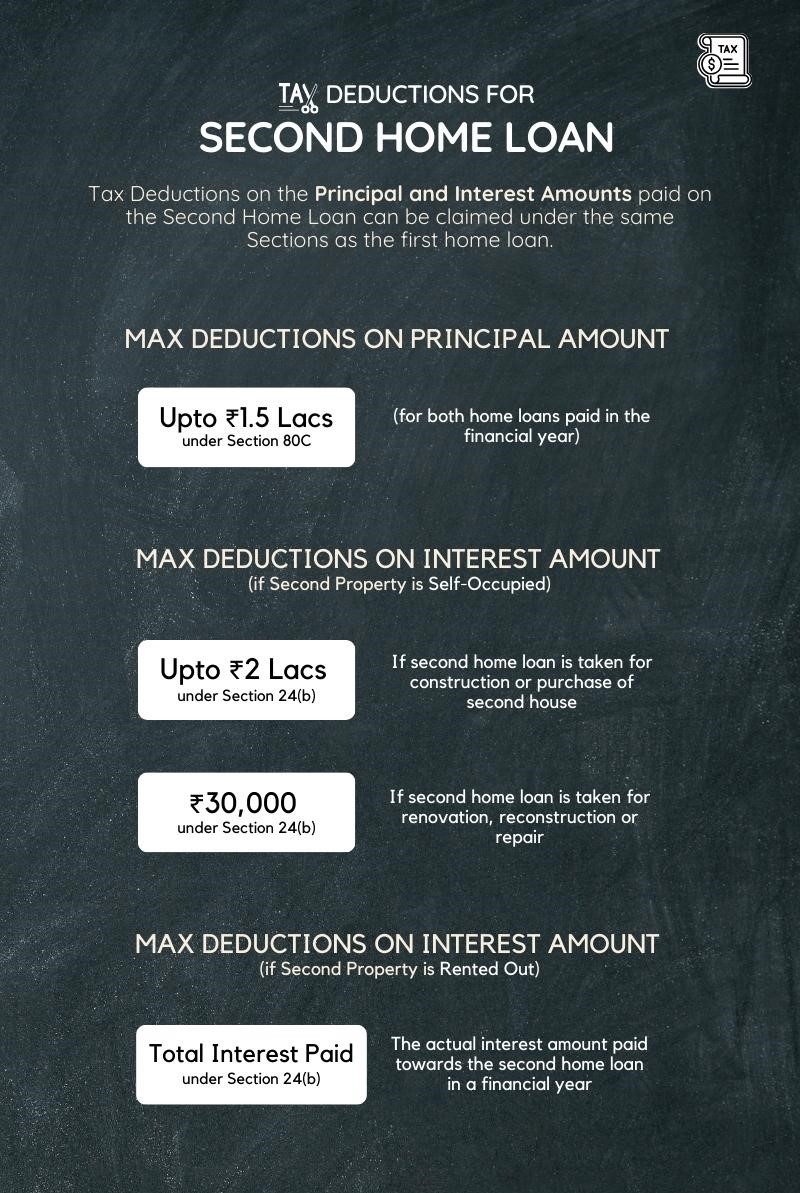

Tax Deductions on Second Home Loan (Purchasing Second Property)

Owning multiple properties is a strategic investment decision. When acquiring a second home loan to purchase an additional property, understanding the tax implications becomes paramount.

To incentivize investment in real estate and stimulate demand in the housing sector, the government allows certain tax deductions even on the second home loan, as explained below.

#1 Second Home Loan Tax Benefits on Principal Amount

As per Section 80C, a maximum amount of ₹1.5 lakh can be claimed on principal repayment made during the financial year for both home loans.

E.g., if the principal repayment is ₹1.8 lakh on the first home loan, and ₹1.4 lakh on the second home loan, the tax benefit on principal repayment during the financial year will be limited to a maximum of ₹1.5 lakhs on both the loans combined.

#2 Second Home Loan Tax Benefits on Interest Deductions

Deductions on the second home loan interest will be applicable as per Section 24(b), which involves a maximum interest deduction of up to ₹2 lakhs. These taxation rules will mainly depend on whether the property is 'Self-occupied' or 'Let out' (rented).

With effect from FY 2020-21, the additional properties owned by a taxpayer are also treated as Self-occupied units (whereas, earlier, they were considered 'Deemed to be let out'). So, for both scenarios wherein the second property can be self-occupied or rented, the tax benefits on interest deductions will be calculated as below:

Scenario 1: If Second Property is Self-occupied or Vacant

If both homes are self-occupied, the limit on tax benefits according to Section 24(b) for interest deductions on the second home loan will be calculated as follows:

-

Maximum deduction on interest = ₹2 lakh, if second home loan was taken on or after 1st April 1999 for construction or purchase of the second house.

-

Maximum deduction on interest = ₹30,000, if second home loan was taken on or after 1st April 1999 for repair, renovation, or reconstruction of the second house.

-

Maximum deduction on interest = ₹30,000, if second home loan was taken before 1st April 1999 for construction, purchase, repair, renovation, or reconstruction of the second house.

If the second property is vacant, it will not be deemed let out, and the same provisions will be followed as above. None of these provisions are available for taxpayers opting for the new tax regime.

Remember: If you are still repaying the first home loan, these limits will also include the interest component of the first home loan.

E.g., If the interest paid during a financial year for the first home loan is ₹1.5 lakh, and for the second home loan is ₹1.2 lakh, then a maximum interest deduction of ₹2 lakh is applicable (if all the necessary conditions are satisfied) during the financial year for both home loan interest.

Scenario 2: If Second Property is Let out

If both the first and second homes are let out, the complete interest repaid on the second home loan can be claimed without any upper limit (i.e., the actual interest paid during a financial year).

If the home loan interest is more than the rental income, the losses of up to ₹2 lakh can be adjusted to other income in the same financial year. Any losses above ₹2 lakh can be carried forward for the next 8 subsequent years to be adjusted against 'Income from Property' and no other income head.

This tax benefit can be availed irrespective of the reason for the second home loan (i.e., whether it was taken for construction, purchase, renovation, repair, etc.) Moreover, this provision is available for both old and new tax regimes.

Also Read: Questions to Ask Real Estate Agents Before Finalizing a House

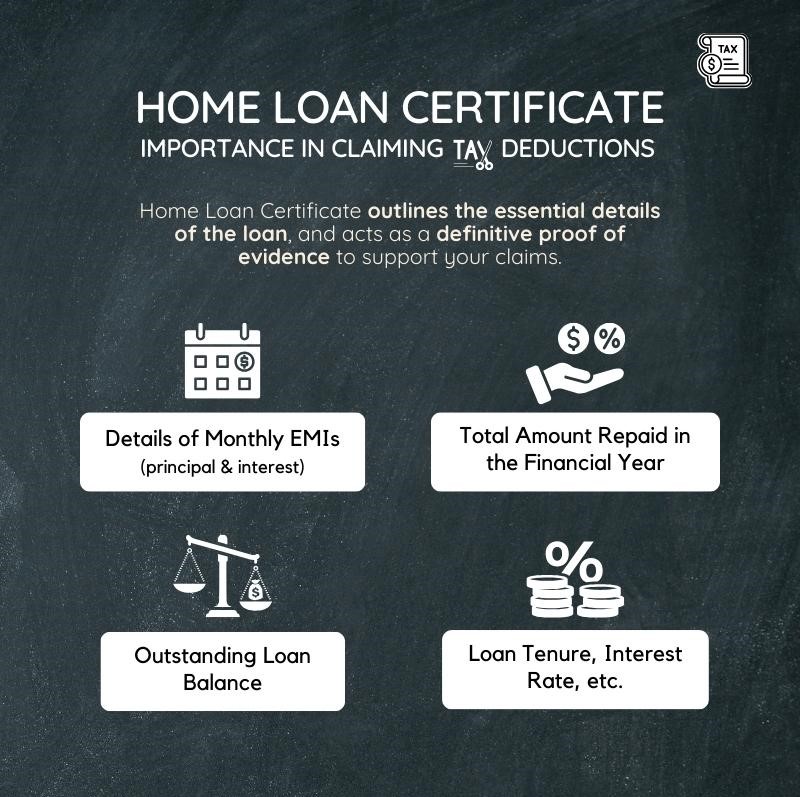

What is Home Loan Certificate & Why is it Crucial?

Home Loan Certificate serves as a record of your repayments and is essential when claiming tax deductions on your home loan.

What is a Home Loan Certificate?

A Home Loan Certificate is an official document provided, usually annually, by the financial (lending) institution and it outlines all the essential details related to your home loan including:

-

Breakdown of monthly EMIs into principal and interest components.

-

Total amount repaid in the given financial year.

-

Outstanding loan balance.

-

Loan tenure, rate of interest, and other vital details.

Its Role in Claiming Tax Benefits

The Home Loan Certificate plays a pivotal role in tax planning for multiple reasons:

-

Valid & Definitive Proof: When claiming tax deductions, you must have definitive proof to substantiate your claims. This certificate serves as valid documentation for the interest and principal amounts you want to claim under Sections 24, 80C, 80EE, and 80EEA.

-

Breakup of Principal and Interest: The Home Loan Certificate provides explicit information about the breakup of your EMI into principal and interest components for accurate filing the IT Returns.

-

Audit Compliance: In case of a tax audit or scrutiny, this certificate serves as an essential piece of evidence supporting your claims.

-

Financial Planning: The certificate also helps you in financial planning by showing the amount of home loan repaid till date and the outstanding loan balance, aiding in decisions like prepayment or loan restructuring.

Home Loan Certificate is not just a piece of paper but a crucial document that facilitates your tax saving journey. Therefore, make sure you promptly get the Home Loan Certificate from your lending institution, preferably every year, and store it securely for future reference.

Mistakes to Avoid when Claiming Tax Benefits on Home Loans

Navigating through home loan tax deductions can be intricate, and a misstep can lead to missed tax benefits or even penalties. Here are some of the most common mistakes, misconceptions, and the importance of various aspects of the home loan process.

#1 Not Being Prepared with the Documentation

Often, taxpayers claim deductions without having essential documents like home loan certificates, which bifurcate principal and interest amounts, or fail to store receipts of stamp duty and registration for Section 80C deductions.

How to Avoid This: Always obtain and preserve a home loan certificate from your lender every financial year. Store all property-related payment receipts securely.

#2 Claiming Deductions Without Properly Defining Ownership

Sometimes co-borrowers, especially in joint home loans, claim deductions without being co-owners.

How to Avoid This: Ensure both the co-borrowers are co-owners of the property as tax benefits are not available for borrowers who are not co-owners. The tax deductions should be claimed in proportion to their ownership share and contribution towards the EMI.

#3 Mistaking Pre-construction Interest Claim can be Done in One Go

Another common error is attempting to claim the entire pre-construction interest in the year the construction completes.

How to Avoid This: Remember that pre-construction interest deductions are spread over 5 years in equal installments and not claimed all at once.

#4 Missing Out on Claiming Deductions in the Successive Years

Some taxpayers forget to claim deductions for the pre-construction interest in subsequent years after initially claiming it.

How to Avoid This: Remember to claim 1/5th of the pre-construction interest every year for five years, starting from the year the construction completes.

#5 Thinking All Components of Home Loan are Deductible

A prevalent misconception is believing that the entire EMI (principal + interest) is tax-deductible. In reality, only the interest component can be claimed under Section 24, while the principal component falls under Section 80C, each having its own limits.

How to Avoid This: Do proper research before claiming tax deductions and make note of which Sections to apply for in order to get the right deduction.

Make sure to pay the monthly EMIs regularly on time to avoid delaying or defaulting on the loan repayment.

- Consistent defaults may cause the lender to label the loan as 'non-performing asset', jeopardizing your tax benefits.

- Late payments or defaults can also lead to penalties and accumulate more interest, increasing your financial burden.

- Credit Score can be impacted which can affect your future loan and credit card applications.

In conclusion, while home loans offer valuable tax deductions, the responsibility is on the borrower/taxpayer to understand, document, and claim these benefits correctly. Avoiding pitfalls and being diligent about your obligations ensures that the journey of homeownership remains both rewarding and financially beneficial.

Navigating the financial landscape of home ownership is undoubtedly intricate. Take some time to think about whether it is better to own a home or rent one, as every individual's financial situation and goals are unique.

However, if you do decide to go ahead and buy a new house with the help of a housing loan, make sure to arm yourself with the knowledge and understanding of the various tax benefits on home loans. It's pivotal to remember that while home loans might seem burdensome at a glance, the tax incentives provided by the government can significantly offset this burden. Sections of the Income Tax Act like 80C, 24, 80EE, and 80EEA, offer substantial financial advantages to homeowners which can help make substantial savings on your annual tax. Understanding and ensuring compliance with required documentation like Home Loan Certificate will ensure your journey of owning a home will feel more rewarding by effectively reducing your tax liabilities and helping you save money.

To maximize the benefits and to ensure you're making the most of every opportunity, consulting with a tax advisor can prove invaluable. Personalized advice can not only help you tap into the full potential of available tax benefits but also strategize for a financially sound future.

In essence, owning a home is a dream for many, and the Indian tax system supports this aspiration by providing generous tax benefits on home loans. So, as you step into or continue your home ownership journey, remember that with the right knowledge and guidance of the available housing loan tax benefit, it can be both a fulfilling and financially savvy venture.